Camping World has shifted its financial strategy away from external capital reliance and toward internal cash preservation, emphasizing liquidity discipline and accelerated inventory velocity. By the end of fiscal year 2025, the company reported $215 million in cash on hand, reinforcing its near‑term liquidity position (Camping World Holdings, 2026).

Handling Cash Flow Problems

Across the available sources, management addresses cash flow constraints and liquidity needs through four primary corrective mechanisms:

-

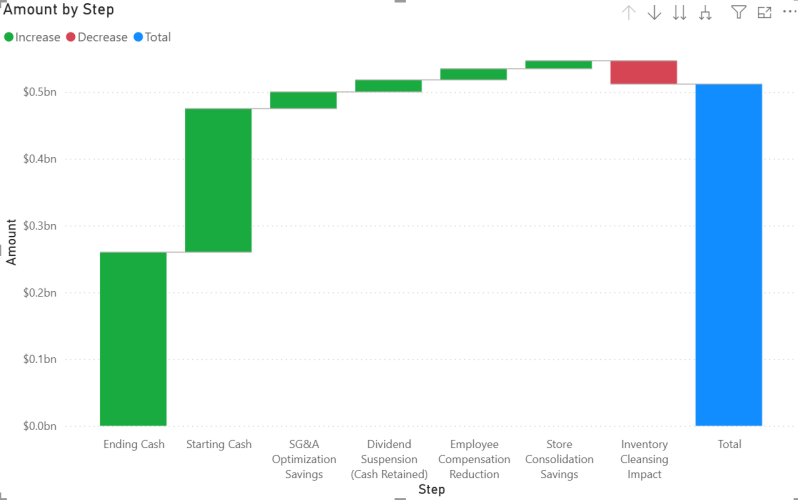

Inventory Velocity & “Cleansing” — Management adopted a “strict and at times, aggressive” approach to liquidating aged Model Year 2025 units, which represented 18% of new inventory at year‑end (Camping World Holdings, 2026). The company aims to raise new‑unit turns from 1.7 to 2.2–2.4, improving working‑capital efficiency. This accelerated turnover is expected to create a $35 million EBITDA headwind in the first half of 2026 (Camping World Holdings, 2026).

-

Dividend Suspension — In February 2026, the Board suspended the quarterly cash dividend to retain operating free cash flow for deleveraging and to maintain strategic “dry powder” for future capital deployment (Camping World Holdings, 2026).

-

SG&A Optimization — To counter margin pressure, management executed $25 million in annualized SG&A reductions, including a $16.7 million decrease in non‑commission employee cash compensation (Camping World Holdings, 2026).

-

Portfolio Optimization — The company consolidated 17 store locations in 2025 to reduce fixed overhead and improve cost efficiency across its nearly 200‑location footprint (RV Business, 2026).

Conditions for Financial Backing and Capital Development

Camping World allocates capital for growth initiatives such as acquisitions or facility upgrades only when specific financial thresholds and strategic criteria are met:

-

Deleveraging Targets — Management identified leverage reduction as a prerequisite for future capital deployment. Net debt leverage stood at 5.7x at the end of 2025, with goals of sub‑4.7x in 2026 and sub‑4x by 2027 (Camping World Holdings, 2026). As evidence of commitment, the company repaid $50 million in long‑term debt early in 2026.

-

Strict Acquisition Criteria — M&A backing is reserved for deals with low rent factors, manageable goodwill, and the ability to add incremental brands to the portfolio (Camping World Holdings, 2026).

-

Internal Profitability Benchmarks — Capital is prioritized for high‑margin segments such as Good Sam, which achieved record revenue in 2025, and Service departments, which maintain margins above 60% (RV Business, 2026).

References

- RV Business. (2026, February 25). Camping World reports $6.4 billion in revenue for 2025. https://rvbusiness.com/camping-world-reports-6-4-billion-in-revenue-for-2025/

- Camping World Holdings, Inc. (n.d.). Overview. https://investor.campingworld.com/overview/default.aspx

AI Disclosure

AI‑assisted tools were utilized in the preparation of this document to streamline drafting, improve clarity, and support data interpretation. These tools functioned as aids only; all substantive decisions, analyses, and final content were reviewed and approved by the author to ensure accuracy, reliability, and compliance with organizational standards.

Add comment

Comments